Australian environmental markets

On this page

- ACCU and Safeguard Mechanism credit unit (SMC) market dynamics summary

- Safeguard Mechanism progress

- Safeguard surrenders drive ACCU holdings

- Generic ACCU and SMC spot prices

- ACCU issuances and project registrations

- Development of new methods continues

- Non-safeguard ACCU cancellations

- Other market developments

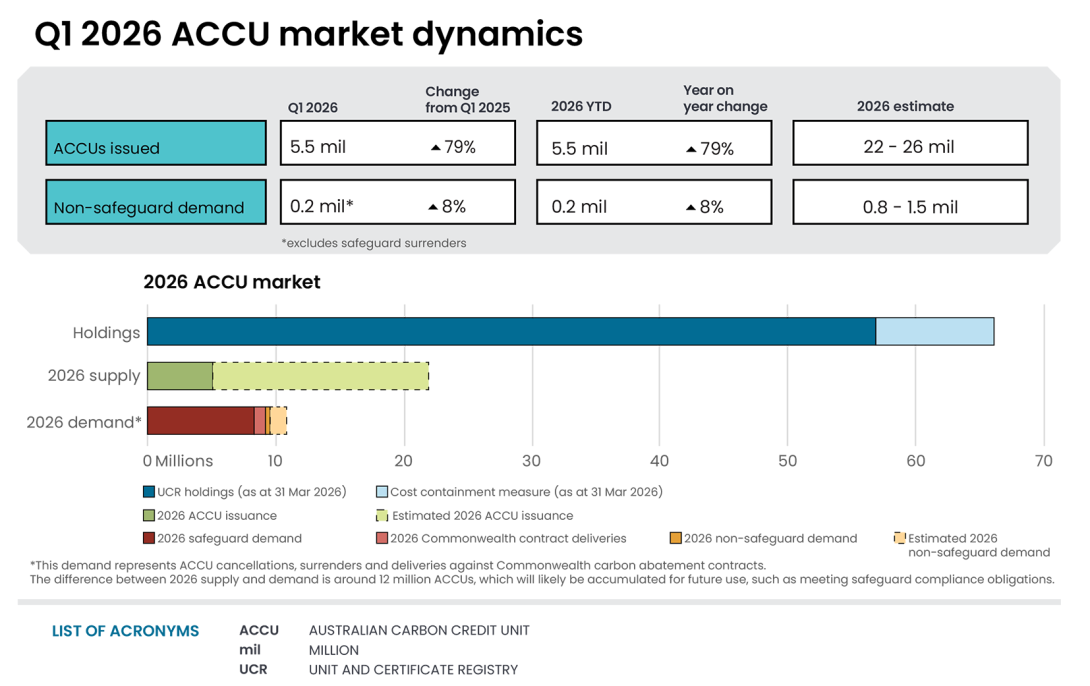

Australian carbon credit unit (ACCU) and Safeguard Mechanism credit unit (SMC) market dynamics summary

| ACCU | Supply | Demand |

|---|---|---|

| Balance carried forward from Q4 2025 | 60.7 m | - |

| ACCU supply | +5.5 m | - |

| ACCU Scheme contract deliveries* | - | -0.7 m |

| Safeguard surrenders | - | -8.8 m |

| Non-safeguard cancellations | - | -0.2 m |

| Net balance at the end of Q1 2026 | 56.5 m | |

| Cost containment measure | 5.5 m | |

Notes:

- Totals may not sum due to rounding.

- *This refers to ACCUs delivered under Commonwealth carbon abatement contracts in the quarter. These ACCUs are held in the cost containment measure and are available to eligible Safeguard entities to purchase at a fixed price of $82.68 for 2025-26, rising at the Consumer Price Index plus 2% each year.

| SMC | Supply | Demand |

|---|---|---|

| Balance carried forward from respective period | 6.9 m | - |

| SMC supply | +6.7 m* | - |

| Safeguard surrenders | - | -2.6 m |

| Net balance at the end of Q1 2026 | 11.0 m | |

Note: *SMC issuances generally occur around 31 January following the end of the relevant reporting period. However, there is no legislative deadline to apply for SMCs so issuances can occur throughout the year and across compliance years depending on when the CER receives the application.

Safeguard Mechanism progress

The CER published the outcomes of the 2024-25 compliance period of the Safeguard Mechanism on the statutory deadline of 15 April 2026. The 2024-25 safeguard publication includes the data from the second year of declining baselines. The data shows the Safeguard Mechanism continues to progress well in line with expectations and policy settings. Key highlights include:

- 208 facilities were covered by the Safeguard Mechanism for the 2024-25 reporting period, down from 219 facilities covered in 2023-24. Yearly changes in the number of facilities covered by the Safeguard Mechanism are often reflective of facilities rising and falling above and below the 100,000 tCO2-e Safeguard threshold.

- Total covered emissions from safeguard facilities for 2024-25 were 132.8 million tonnes of carbon dioxide equivalent (Mt CO2-e), a 2.3% reduction from 136.0 Mt CO2-e in 2023-24.

- Total baselines for 2024-25 were 126.2 Mt CO2-e, a 7.3% reduction from 136.1 Mt CO2-e for 2023-24.

- 141 facilities’ net emissions exceeded their baselines in 2024‑25, with a total excess of 13.7 Mt CO2‑e, an increase from 9.2 Mt CO2-e excess in 2023-24.

- To manage excess emissions, entities surrendered 10.8 million ACCUs and 2.6 million SMCs.

- A total of 6.7 million SMCs were issued to 54 responsible emitters for 2024-25, a 19.4% reduction from 8.3 million in 2023-24.

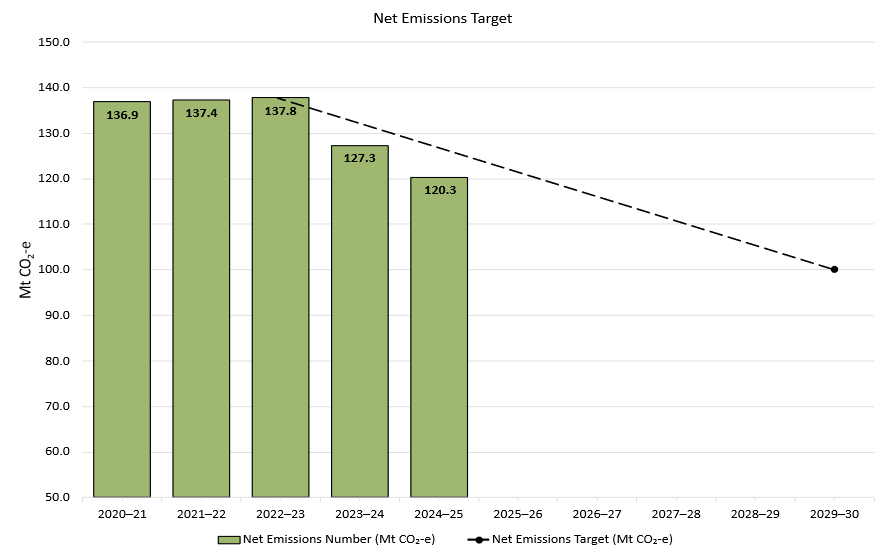

The 2024-25 compliance year was the second since the Safeguard Mechanism reform in 2023. The cumulative impact of the scheme since its reform includes a total reduction in covered emissions of 5.8 Mt CO2-e across the 2 completed years, with net emissions falling 17.5 Mt CO2-e. This tracks below the trajectory for the scheme’s objective of less than 100 Mt CO2-e of net emissions in the 2029-30 financial year. Baselines have reduced by a total of 45.4 Mt CO2-e in the 2 years. This year was the first time that total covered emissions were higher than total baselines, meaning ‘aggregate headroom’ - the difference between total covered emissions and total baselines - has been removed.

Transitioning to lower emissions production requires time and investment that may not be completed at this point. ACCU and SMC surrender act as a flexibility measure until lower emissions production can be fully achieved. Net emissions numbers decreasing in the 2 years of the reformed Safeguard Mechanism is a sign that the mechanism is working as intended, with emissions moving downward since 2022-23.

Emitters need to sustain this good early progress by investing in available technologies and continuing to support research and develop in sectors where these are still emerging.

Progress towards net emissions target of ≤ 100 Mt CO2-e in 2029–30

Note: This figure is not interactive.

Description

This figure shows net emissions from 2020-21 to 2024-25 from Safeguard facilities and the net emissions target from 2022-23 to 2029-30 where the net emissions target is 100 Mt CO2-e.

Small print

Net emissions from eligible facilities under subsection 58B of the Safeguard Rule are not included. For more data on the Safeguard Mechanism, including Safeguard Mechanism credit unit issuance and surrenders, refer to safeguard data.

The government’s review of the Safeguard Mechanism in 2026–27 will consider whether its policy settings are appropriately calibrated. The review will consider a range of matters including the emissions baseline decline rate, coverage arrangements considering any competitiveness issues, the use of offsets beyond 2030 and the suitability of arrangements for emissions-intensive trade-exposed activities.

Safeguard surrenders drive ACCU holdings

Holdings in the UCR fell as expected, with holdings excluding the cost containment measure falling from 60.7 million at the end of 2025 to 56.5 million at the end of Q1 2026. This reduction was driven by surrenders made by safeguard entities. Holdings in safeguard and safeguard-related accounts fell by 2.1 million but still make up 66% of all ACCU holdings. In addition, following the announcement of the Permanent exit arrangements for holders of carbon abatement contracts (CACs), around 0.7 million ACCUs were delivered to the Commonwealth over the same period, increasing the volume in the cost containment measure to 5.5 million ACCUs. CER analysis shows around 12% of ACCUs are held by overseas accounts (see International ACCU holdings).

Description

This figure shows ACCU holdings in Unit and Certificate Registry (UCR) accounts as of 31 March 2026 by market participation and the cost containment measure quarterly over time.

Small print

Totals may not sum due to rounding. ACCU holdings data excludes ACCUs held in accounts controlled by the Australian Government for scheme administration purposes. Historical values may change retrospectively due to changes in the classification of UCR accounts as new information becomes available. UCR accounts are categorised based on their main activity, as some accounts may fulfill conditions for multiple categories.

Holdings have not been categorised prior to 2019 as the categories cannot be mapped.

Category

ACCU project proponent

An account holder is connected to one or more ACCU Scheme projects. The connection to projects has been determined based on the available project information. Entities may have linkages to projects that have not been disclosed to the Clean Energy Regulator.

Safeguard

Account holders are safeguard entities that control a single account, or in cases where safeguard entities control multiple accounts, only those that have surrendered ACCUs for safeguard compliance purposes or have specified a facility are included. Some safeguard accounts also engage in trading activity, which may result in holding fluctuations in this category.

Safeguard related

Account holders are companies, such as subsidiaries, that are related to registered safeguard entities. These accounts do not specify a facility or have not surrendered ACCUs for safeguard compliance purposes. These ACCU holdings may be used for future safeguard compliance purposes.

Intermediary

An account holder’s primary operation is to facilitate the trading of ACCUs between the supply and demand sides of the market. This also includes accounts that have accumulated ACCUs through the secondary market without known compliance obligations, offset use, or carbon trading/offset services.

Government

Account holders are government entities that are accumulating for voluntary or compliance purposes.

Business

Account holders do not have a direct link to ACCU Scheme projects. Account holders include participants that are accumulating for voluntary purposes.

Total holdings

For the ACCU scheme, total holdings in the Unit and Certificate Registry are the sum of ACCUs held in ACCU project proponent, safeguard, safeguard related, intermediary, government, and business accounts and exclude accounts controlled by the Clean Energy Regulator such as the cost containment measure.

Cost containment measure

ACCUs that have been delivered under Commonwealth carbon abatement contract milestones after 12 January 2023. These ACCUs will be available to eligible safeguard entities under the cost containment mechanism. This is not included in total holdings.

Following the issuance of 6.7 million SMCs and the surrender of 2.6 million SMCs, SMC holdings in the UCR rose to 11.0 million. Safeguard and safeguard related accounts currently hold 95% of SMCs in the UCR with the remainder being held by intermediary accounts.

Description

This figure shows SMC holdings in Unit and Certificate Registry (UCR) accounts by market participation quarterly over time.

Small print

Totals may not sum due to rounding. Historical values may change retrospectively. This is due to changes in the classification of UCR accounts as new information becomes available. UCR accounts are categorised based on their main activity, as some accounts may fulfil conditions for multiple categories.

Category definitions

Safeguard

Account holders are safeguard entities that control a single account, or in cases where safeguard entities control multiple accounts, only those that have surrendered SMCs for safeguard compliance purposes or have specified a facility are included. Some safeguard accounts also engage in trading activity, which may result in holding fluctuations over time.

Intermediary

An account holder’s primary operation is to facilitate the trading of SMCs between the supply and demand sides of the market. This also includes accounts that have accumulated SMCs through the secondary market without known compliance obligations.

Safeguard related

Account holders are companies, such as subsidiaries, that are related to registered safeguard entities. These accounts do not specify a facility or have not surrendered SMCs for safeguard compliance purposes. These SMC holdings may be used for future safeguard compliance purposes.

ACCU project proponent

An account holder is connected to one or more ACCU Scheme projects. The connection to projects has been determined based on the available ACCU Scheme project information. Entities may have linkages to ACCU Scheme projects that have not been disclosed to the Clean Energy Regulator.

Safeguard compliance remains the main driver for ACCU demand with Q1 2026 setting a record for surrenders. The overwhelming majority of ACCUs and SMCs surrendered during the quarter were surrendered for the 2024-25 reporting period, with <0.1% being surrendered for the 2023‑24 reporting period because of National Greenhouse and Energy Reporting (NGER) resubmissions resulting in higher excess positions.

Description

This figure shows ACCU and SMC safeguard surrenders by quarter and the annual total over time.

Small print

Safeguard surrenders are made by safeguard entities to meet Safeguard Mechanism compliance. For more data on the Safeguard Mechanism, including Safeguard Mechanism credit unit issuance and surrenders, refer to safeguard data.

Description

This figure shows ACCU holdings in Australian National Registry of Emissions Units (ANREU) accounts as of 31 March 2026 by location of the account quarterly over time.

Note

Location of holdings are classified based on the self-provided addresses of ACCU account holders. They do not reflect the location of the ultimate parent company of the account holder.

Small print

Totals may not sum due to rounding. ACCU holdings data excludes ACCUs held in accounts controlled by the Australian Government for scheme administration purposes. The location of ANREU accounts is based on self-provided addresses. They do not reflect the location of the ultimate parent company of the account holder.

Generic ACCU and SMC spot prices

The generic volume-weighted ACCU spot price was relatively flat over the quarter, falling from $36.60 at the end of 2025 to $36.28 at the end of Q1 2026. Market intelligence suggests that safeguard entities have been in engagement with the market since the previous 2024-25 compliance deadline, with many entities having acquired ACCUs well before the 31 March 2026 compliance deadline. As a result, there have been fewer major price fluctuations in the lead up to the end of Q1 2026 than in some previous years. Post-quarter the ACCU spot price rose to $37.50 on 15 May 2026.

SMC spot prices followed ACCUs closely with a maximum price difference of $0.17 in late February. Liquidity in the SMC market remains thin, with market intelligence pointing to a supply constrained market.

Generic Australian carbon credit unit (ACCU) and Safeguard Mechanism credit unit (SMC) volume weighted average spot price

Note: This figure is not interactive.

Description

This figure shows the volume weighted average of the generic ACCU and SMC spot prices over time.

Small print

The generic spot price refers to the daily volume weighted average price of spot trades for ACCUs with an unspecified method and spot trades for SMCs. Spot trade data is compiled from trades reported by Jarden and CORE markets, and may not be comprehensive. Prices are shown from 31 December 2020 to 15 May 2026. The last quarterly reported daily volume weighted average spot prices for generic ACCUs and SMCs are labelled.

ACCU issuances and project registrations

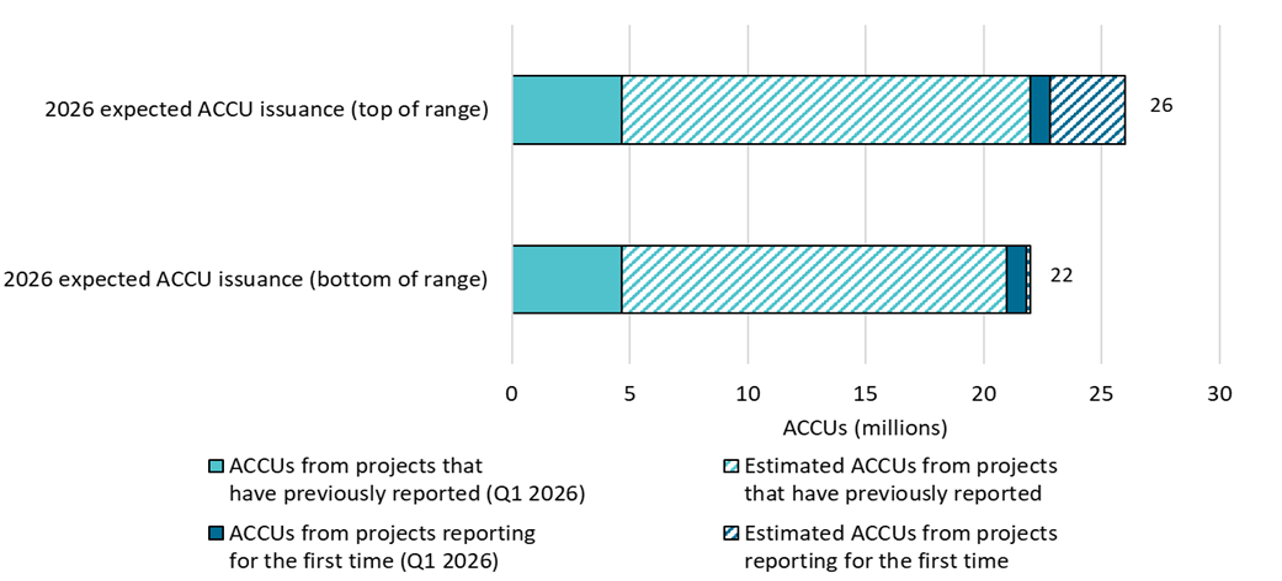

Issuance in Q1 2026 reached a record 5.5 million ACCUs, beating the previous record of 3.8 million in 2024. ACCU issuance is currently on track to meet the CER’s estimated range of 22 to 26 million. Projects claiming for the first time in Q1 2026 were issued 0.8 million ACCUs. This larger issuance was driven by a total of 3.7 million ACCUs issued to vegetation method projects, with 89% of vegetation ACCUs issued to human‑induced regeneration (60%) and environmental plantings projects (29%). The high issuance to environmental plantings projects was driven by a few large projects claiming ACCUs covering multiple years of abatement and several projects reporting for the first time. Issuance to waste projects were lower than usual in Q1 2026. Due to the expiring source separated organic waste method, our waste assessment team prioritised registering projects under this method over processing issuances.

In Q1 2026, 69 ACCU Scheme projects were registered, lower than the 90 in the same period last year. The result for the quarter is in line with the Q1 average this decade; Q1 2025 saw higher registrations for the waste and industrial fugitives methods ahead of their sunsetting.

Description

This figure shows ACCUs issued by method type and the annual total over time. This includes ACCUs that have been relinquished.

Small print

ACCU issuance follows a seasonal pattern for certain method types, including industrial fugitive and savanna fire management.

Other includes energy efficiency, industrial fugitives, agriculture, carbon capture, transport and facilities method types.

Description

This figure shows registered projects under the ACCU Scheme by method type and the annual total over time.

Small print

The 'agriculture' method type has been segregated into 'agriculture - soil carbon' and 'agriculture - other' to highlight growth in the soil carbon sector. The 'agriculture - soil carbon' method includes the ‘measurement of soil carbon sequestration in agricultural systems' method, the ‘sequestering carbon in soils in grazing systems’ method and the 'estimation of soil carbon sequestration using measurement and models' method.

Other includes energy efficiency, agriculture - other, savanna fire management, transport, industrial fugitives, facilities and carbon capture method types.

Revoked projects are excluded.

For more detail on registered projects, refer to the project register.

Estimated Australian carbon credit unit (ACCU) issuances (in millions) in 2026

Note: This figure is not interactive.

Description

This figure shows the range of expected ACCU issuances for 2026 by category. Expected issuances were calculated using data as at 31 March 2026.

Small print

Category details:

A) ACCUs from projects that have previously reported

This is an estimate based on factors such as the typical timing and volume of ACCUs per claim. This category factors in ACCUs from applications on hand at the start of 2026.

B) ACCUs from projects reporting for the first time

This is an estimate based on factors such as the typical timing and volume of first issuance. This category is the main driver of uncertainty for the 2026 estimate.

Development of new methods continues

The Department of Climate Change, Energy, the Environment and Water (DCCEEW) are continuing work on developing new ACCU Scheme methods as some older methods expired at the end of March.

On 10 April 2026, the Australian Government made 2 new savanna fire management methods. As discussed in the Q2 2025 Quarterly Carbon Markets Report (QCMR), on average, credited abatement for projects under the new method is likely to be higher than under earlier savanna fire management calculators. This reflects the crediting of sequestration in additional carbon pools, enabled by improvements in scientific modelling. One of the new methods includes a novel sequestration bank mechanism, which smooths issuances over projects’ crediting periods (see The sequestration bank in the savanna fire management method: illustrative example).

The CER will continue to monitor the abatement outcomes of projects under these new methods, which can vary depending on factors such as rainfall zones. The new savanna methods, along with other methods in development, will continue to support ACCU supply well into the 2030s.

As noted in the Emissions Reduction Assurance Committee’s (ERAC’s) meeting summary for 4 March 2026, the development of the Improved Native Forestry Management (INFM) method is progressing well. ERAC has identified several issues relating to carbon leakage, baselines, and data transparency that remain to be addressed to ensure the method meets the Offsets Integrity Standards.

On 31 March 2026 the methods high efficiency commercial appliances 2015 and refrigeration and ventilation fans 2015 expired, meaning no more projects can be registered under these methods. Due to low or no uptake, these methods are not receiving any further action. The source separate organic waste 2016 method also expired on 31 March 2026. Activities covered by the expired method will be considered in the development of the new alternative waste treatment method which has been identified for proponent‑led method development.

Public consultation on the proposed Integrated Farming and Land Management (IFLM) method closed on 9 March 2026. The department and ERAC are currently considering the feedback received and next steps associated with the method’s development.

More information on these and other methods can be found on DCCEEWs ACCU method tracker.

Description

This figure shows changes in the sequestration bank and release for a hypothetical savanna fire management project.

Small print

The hypotethical project has sequestered 500 tCO2-e in the sequestration bank. Half of the abatement sequestered in each calendar year is added to the bank. The rate of release is inversely proportional to the number of years left in the project’s crediting period.

Non-safeguard ACCU cancellations

In Q1 2026 0.2 million ACCUs were cancelled for non-safeguard purposes, 8% higher than the same period last year. Non-safeguard cancellations are on track to meet the CER’s estimated range of 0.8 to 1.5 million. Entities are known to cancel on a variable schedule, with some entities cancelling for the end of a financial year, while others cancel for the end of a calendar year.

Description

This figure shows ACCU non-safeguard (voluntary, compliance, and government) cancellations quarterly and the annual total over time.

Small print

ACCU cancellations exclude deliveries against Commonwealth carbon abatement contract milestones, surrenders for safeguard purposes, and transfers to the Commonwealth Regulatory Additionality Holding Account. This classification system is uniform across ACCU and large-scale generation certificate (LGC) cancellations.

Category definitions

Voluntary

Cancellations made against voluntary certification programs and any sort of organisational emissions targets.

Compliance

Cancellations made by private organisations and corporations for compliance or obligations against municipal, local, state and territory government laws, approvals, or contracts. For example, cancellations to meet Environmental Protection Authority requirements.

Government

Cancellations by or on behalf of government entities. For example to offset emissions from vehicle fleets or meet voluntary emissions reduction targets.

Other market developments

Nature Repair Market update

The Nature Repair Market is being designed to support voluntary action on nature repair as well as providing a source of offsets.

Under the replanting native forest and woodland ecosystems 2025 method, as of 27 May 2026, 2 projects have been registered, with other potential proponents actively working with the CER to support registration of additional projects.

Between 20 April and 4 May 2026 DCCEEW conducted targeted consultation on policy settings to give effect to amendments to the Nature Repair Act 2023 passed by the Parliament on 28 November 2025 as part of the Australian Government’s Environment Protection Reform Bills. The reforms allowed for methods to specify whether biodiversity projects can be used as environmental offsets in limited circumstances. Consultation sought feedback on policy settings to enable the Nature Repair Market to supply environmental offsets, the Threatened Species variable biodiversity project characteristic, and proposed operational and administrative changes to the Nature Repair Rules 2024.

The proposed protect and conserve and enhancing native vegetation methods continue to be developed. The Nature Repair Committee plan to undertake statutory consultation on the final proposed methods in 2026.

Further work related to offsets is underway to develop National Environmental Standards and establish the Restoration Contributions Holder, for more information see Stronger environmental protection and restoration.

Product Guarantee of Origin update

DCCEEW continues consultation on new products to be certified under the Product Guarantee of Origin scheme.

The first consultation this year sought feedback on 2 additional hydrogen production pathways (gas reforming, and solid gasification & pyrolysis), and the aluminium production pathway. These consultations closed on 6 February 2026 and further details on this consultation are available at: Public consultation on the Exposure Draft of the Guarantee of Origin Methodology Determination Amendment - Department of Climate Change, Energy, Environment and Water.

A separate consultation on iron ore mining and biogas and biomethane from anaerobic digestion closed on 27 April 2026. Further details on this consultation are available at: Public consultation on the Exposure Draft of the Guarantee of Origin Methodology Determination Amendment (Biogas, Biomethane and Iron Ore) - Department of Climate Change, Energy, Environment and Water.

Emissions accounting methods for these products are expected to be made mid‑year.

The CER is responsible for updating scheme cost recovery arrangements. Public consultation on a cost recovery update to cover new Product Guarantee of Origin methods opened on 13 May and will close on 8 June. It covered 4 additional products – hydrogen by gasification and pyrolysis, biogas and biomethane, and bio-LPG – which were not included in the original Guarantee of Origin Cost Recovery Implementation Statement published in October 2025. The Assistant Minister for Climate Change and Energy will consider feedback received and approve the final updated cost recovery arrangements, which will be published alongside approved methods. A periodic review of whole-of-scheme Guarantee of Origin cost recovery arrangements, separate to this update, is scheduled to commence in the second half of 2026.

International Transaction Log and certified emission reduction units

Certified emission reduction units are Kyoto Protocol carbon credits that represent one tonne of CO2‑e avoided or sequestered by projects registered under the Clean Development Mechanism prior to 2021. Following the end of the Kyoto Protocol ‘true-up’ period in September 2023, the United Nations Framework Convention on Climate Change (UNFCCC) Secretariat’s International Transaction Log (ITL) continued to validate voluntary cancellation transactions for those national registries that continued to support certified emission reduction units, including the ANREU.

At COP30 in November 2025, parties agreed to support the disconnection of the ITL from all national registries on 31 March 2026. Changes to the ANREU system were successfully made to enable voluntary cancellations and internal transfer of certified emissions reduction Units to continue independently of the ITL. No further issuances of units or transfers to external registries will occur.

Approximately 8.5 million certified emission reduction units were still held in ANREU accounts as of 31 March 2026. These continue to be used for voluntary purposes, both within Australia and overseas. A total of 1.0 million certified emission reduction units were voluntarily cancelled by ANREU accounts in Q1 2026, an increase from both the 0.4 million units cancelled in the previous quarter, and the 0.7 million cancelled in Q1 2025.

The Clean Energy Regulator will migrate certified emission reduction units from the ANREU to the UCR in June 2026. As the number of certified emission reduction units and the number of ANREU accounts holding them are decreasing, there will be a more streamlined approach to the management of certified emission reduction units using the Notify the Regulator form via Online Services. Transaction and holdings records will be securely and irrefutably held in the Unit and Certificate Registry, and statements will be provided by email.

Carbon Credits and Other Legislation Amendment (Integrity and Transparency) Bill Consultation

DCCEEW released a consultation paper on the Carbon Credits and Other Legislation Amendment (Integrity and Transparency) Bill amendments on 30 April 2026. The proposed changes include changes in response to the Independent Review of ACCUs and Climate Change Authority ACCU Scheme reviews, including integrity and transparency improvements.

The amendments to both the Carbon Credits (Carbon Farming Initiative) Act 2011 (CFI Act) and the National Greenhouse and Energy Reporting Act 2007 (the NGER Act) include changes to:

- strengthen ACCU Scheme consent requirements by recognising registered native title claimants as eligible interest holders and requiring up-front and staged consent for projects on land that is recognised as native title land, or subject to native title claims.

- enable the existing ACCU Scheme ERAC to evolve into the new Carbon abatement Integrity Committee (CAIC).

- clarify the governance arrangements for proponent-led method development in the ACCU Scheme.

- create new Ministerial powers to manage critical integrity risks the ACCU Scheme could face in the future.

- encourage greater investment and participation in research and development into new emissions reduction opportunities for the ACCU Scheme.

- enhance the CER’s compliance and publication powers to ensure ongoing integrity and transparency of the ACCU Scheme.

- simplify and streamline the ACCU Scheme administration.

- enhance the transparency and administration of the NGER Scheme.

Consultation closed on 22 May 2026. Feedback will inform the final proposed legislation package.

Integrity and transparency updates

As part of our ongoing work to increase transparency and provide carbon markets with more information about the schemes we administer, we:

- published the outcomes for the 2024-25 Safeguard reporting period.

- are releasing a new QCMR Methods document concurrently with this report. This living document consolidates the approach behind QCMR projections in one place, providing interested readers with more technical information about the data and methods used in the QCMR.

- updated our website on interoperability with the Unit and Certificate Registry to include:

- draft principles of interoperability that guide CER’s implementation of interoperability and sets expectations for third parties connecting to our systems.

- prototype interoperability models that describe the potential Application Programming Interface (API) connections between external systems and our registers and registries.

- published a summary of responses to our consultation on improvements to the ACCU project and contract register. Work to improve the content and presentation of the register will continue during 2026. This includes migrating the register to data services and changing the data.