Australian environmental markets

On this page

- ACCU and Safeguard Mechanism credit unit (SMC) market dynamics summary

- Safeguard Mechanism

- Permanent exit arrangements for fixed delivery Commonwealth carbon abatement contracts

- 2025 ACCU issuances and project registrations

- 2026 ACCU issuances expected to be between 22 and 26 million

- Non-safeguard ACCU cancellations

- Generic ACCU and SMC spot prices

- Nature Repair Market update

- Integrity and transparency update

ACCU and Safeguard Mechanism credit unit (SMC) market dynamics summary

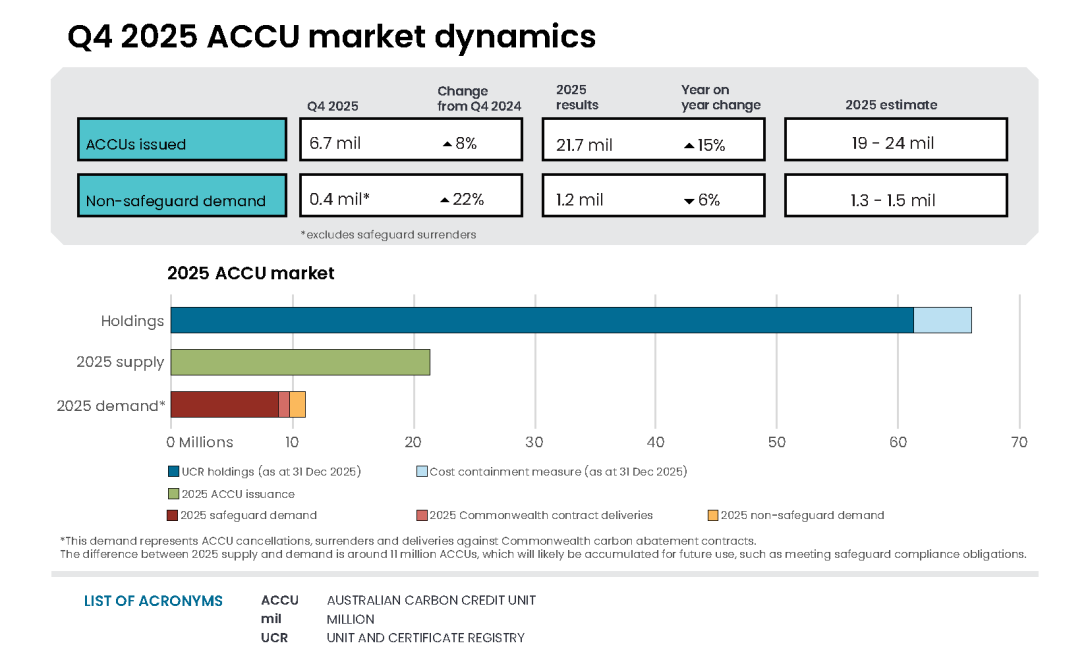

| Q4 2025 | 2025 annual change | |||

|---|---|---|---|---|

| ACCU | Supply | Demand | Supply | Demand |

| Balance carried forward from respective period | 56.8m | - | 49.9m | - |

| ACCU supply | +6.7m | - | +21.7m | - |

| ACCU Scheme contract deliveries* | - | -0.4m | - | -0.9m |

| Safeguard surrenders | - | -1.9m | - | -8.7m |

| Non-safeguard cancellations | - | -0.4m | - | -1.2m |

| Net balance at the end of Q4 2025 | 60.7m | |||

| Cost containment measure | 4.8m | |||

Notes:

- Totals may not sum due to rounding.

- * This refers to ACCUs delivered under Commonwealth carbon abatement contracts in the quarter. These ACCUs are held in the cost containment measure and are available to eligible Safeguard entities to purchase at a fixed price of $82.68 for 2025-26, rising at the Consumer Price Index plus 2% each year.

| Q4 2025 | 2025 annual change | |||

|---|---|---|---|---|

| SMC | Supply | Demand | Supply | Demand |

| Balance carried forward from respective period | 6.9m | - | - | - |

| SMC supply | +<0.1m** | - | +8.3m | - |

| Safeguard surrenders | - | -<0.1m | - | -1.4m |

| Net balance at the end of Q4 2025 | 6.9m | |||

Notes:

- ** SMC issuances generally occur around 31 January following the end of the relevant reporting period. However, there is no legislative deadline to apply for SMCs so issuances can occur throughout the year and across compliance years depending on when the CER receives the application.

Safeguard Mechanism

The second compliance year of the reformed Safeguard Mechanism continues smoothly.

In Q4 2025, the CER published the safeguard preliminary data insights, to provide an early overview of Safeguard Mechanism outcomes and key market data for the 2024-25 reporting period. The report indicated a cumulative excess of 13.7 million tonnes of carbon dioxide equivalent (CO2-e). Excess emissions can be managed by surrendering ACCUs or SMCS, or by applying and being approved to use flexibility arrangements, including borrowing baseline (with interest) from the following year, or using a multi-year monitoring period. As usual this preliminary data is subject to change and does not fully consider the approval of any ongoing flexibility measure applications, such as trade-exposed baseline adjustments.

The CER will continue with scheme administration including SMC issuances. Following the compliance deadline on 1 April 2026, the full results of the 2024-25 reporting year will be published on 15 April 2026.

Safeguard demand for ACCUs continues to grow

As responsible emitters can manage excess emissions by surrendering ACCUs or SMCs, safeguard compliance remains the main driver for ACCU demand. In Q4 2025, 1.9 million ACCUs were surrendered for safeguard compliance. Of these, 0.2 million was for 2023-24 compliance through an enforceable undertaking and the remaining 1.7 million was for 2024-25 compliance.

ACCU holdings increase ahead of Safeguard Mechanism surrenders

ACCU holdings, excluding the cost containment measure, rose by 3.9 million during Q4 2025, reaching 60.7 million at the end of 2025. This is an annual increase of 10.8 million compared to holdings at the end of 2024. Safeguard and safeguard-related accounts were the main drivers, with their holdings increasing by 10.2 million in 2025 to a total of 39.5 million ACCUs. This represents around two-thirds of total ACCU holdings at the end of Q4 2025. Holdings are categorised based on currently available information for accounts, so breakdowns should be treated as estimates.

As observed in 2025, ACCU holdings are expected to dip in Q1 2026 before continuing to increase over the rest of the year. This is mainly due to safeguard entities managing their excess emissions ahead of the 31 March 2026 compliance deadline for the second year of the reformed Safeguard Mechanism.

The consensus projection of market analysts is that compounding safeguard baseline reductions will result in net ACCU holdings beginning to decline in the later part of this decade. Annual safeguard demand is projected to outpace annual ACCU supply as we approach 2030, seeing the ACCU market tighten.

Description

This figure shows ACCU holdings in Unit and Certificate Registry (UCR) accounts as of 31 December 2025 by market participation and the cost containment measure quarterly over time.

This figure is interactive. Hover over/tap each data point to see the ACCU holdings in millions. Click/tap on the items in the legend to hide/show data in the figure.

Small print

Totals may not sum due to rounding. ACCU holdings data excludes ACCUs held in accounts controlled by the Australian Government for scheme administration purposes. Historical values may change retrospectively due to changes in the classification of UCR accounts as new information becomes available. UCR accounts are categorised based on their main activity, as some accounts may fulfil conditions for multiple categories.

Holdings have not been categorised prior to 2019 as the categories cannot be mapped.

Category definitions

ACCU project proponent

An account holder is connected to one or more ACCU Scheme projects. The connection to projects has been determined based on the available project information. Entities may have linkages to projects that have not been disclosed to the Clean Energy Regulator.

Safeguard

Account holders are safeguard entities that control a single account, or in cases where safeguard entities control multiple accounts, only those that have surrendered ACCUs for safeguard compliance purposes or have specified a facility are included. Some safeguard accounts also engage in trading activity, which may result in holding fluctuations in this category.

Safeguard related

Account holders are companies, such as subsidiaries, that are related to registered safeguard entities. These accounts do not specify a facility or have not surrendered ACCUs for safeguard compliance purposes. These ACCU holdings may be used for future safeguard compliance purposes.

Intermediary

An account holder’s primary operation is to facilitate the trading of ACCUs between the supply and demand sides of the market. This also includes accounts that have accumulated ACCUs through the secondary market without known compliance obligations, offset use, or carbon trading/offset services.

Government

Account holders are government entities that are accumulating for voluntary or compliance purposes.

BusinessAccount holders do not have a direct link to ACCU Scheme projects. Account holders include participants that are accumulating for voluntary purposes.

Total holdings

For the ACCU Scheme, total holdings in the Unit and Certificate Registry are the sum of ACCUs held in ACCU project proponent, safeguard, safeguard related, intermediary, government, and business accounts and exclude accounts controlled by the Clean Energy Regulator such as the cost containment measure.

Cost containment measure

ACCUs that have been delivered under Commonwealth carbon abatement contract milestones after 12 January 2023. These ACCUs will be available to eligible safeguard entities under the cost containment mechanism. This is not included in total holdings.

At the end of Q4 2025, SMC holdings remained stable at 6.9 million. Most SMC activity is expected in Q1 each year. Most SMC issuances typically occur around 31 January and most SMC surrenders typically occur in the lead up to 31 March compliance deadline. The vast majority (96%) of SMCs continue to be held by safeguard and safeguard-related accounts.

Permanent exit arrangements for fixed delivery Commonwealth carbon abatement contracts

On 3 December 2025, the Australian Government announced the implementation of a permanent exit arrangement for fixed delivery Commonwealth carbon abatement contracts. These arrangements aim to resolve the management of fixed delivery carbon abatement contracts by providing an alternative pathway for sellers to meet their obligations. Under the permanent arrangements, eligible sellers will receive a 60% discount on their exit payment fees if they deliver at least 25% of the outstanding volume of ACCUs as of 1 January 2025. The permanent exit arrangement recognises market and policy settings have changed since the introduction of carbon abatement auctions and fixed delivery contracts in 2015.

ACCUs delivered under contract will still be paid the contract price. In total for 2025, 0.9 million ACCUs were delivered with almost half (0.4 million) delivered after the announcement of the permanent exit arrangements. At the end of Q4 2025, the cost containment measure held 4.8 million ACCUs. Contract deliveries are expected to increase in 2026 compared to 2025 as contract holders service the 25% minimum delivery under the permanent exit arrangement.

Sellers and authorised representatives must complete an expression of interest by 30 June 2026 before the permanent exit arrangement begins on 1 July 2026.

2025 ACCU issuances and project registrations

ACCU issuances in 2025 reached a record 21.7 million, with 6.7 million ACCUs issued in Q4. This is in line with our 2025 estimate of 19-24 million and is 2.9 million higher than 2024 issuances. Higher issuances were driven by vegetation projects with 2.5 million more ACCUs issued in 2025 than in 2024.

Of the 21.7 million ACCUs issued in 2025:

- 17.3 million were issued to projects that have previously reported.

- This was slightly below our expected range of 17.7 to 18.7 million.

- 4.4 million were issued to projects reporting for the first time.

- This was within our expected range of 1.5 to 5.5 million.

Description

This figure shows ACCUs issued by method type and the annual total over time. This includes ACCUs that have been relinquished.

This figure is interactive. Hover over/tap each bar to see the quarterly ACCU issuance in millions. Hover over/tap on the line to see the annual ACCU issuance. Click/tap on the items in the legend to hide/show data in the figure.

Small print

ACCU issuance follows a seasonal pattern for certain method types, including industrial fugitive and savanna fire management.

Other includes energy efficiency, industrial fugitives, agriculture, carbon capture, transport and facilities method types.

In 2025, 407 ACCU Scheme projects were registered. This is comparable to the 421 ACCU Scheme projects registered in 2024. Plantation Forestry saw the biggest increase in registrations, reaching a record 100 registrations in 2025 compared to 66 in 2024. This made Plantation Forestry the second most registered method in 2025, behind Estimation of Soil Organic Carbon Sequestration using Measurement and Models, and ahead of Reforestation by Environmental or Mallee Plantings. These figures exclude revoked projects.

Description

This figure shows registered projects under the ACCU Scheme by method type and the annual total over time.

This figure is interactive. Hover over/tap each bar to see the number of projects registered quarterly. Hover over/tap on the line to see the annual total of project registrations. Click/tap on the items in the legend to hide/show data in the figure.

Small print

The 'agriculture' method type has been segregated into 'agriculture - soil carbon' and 'agriculture - other' to highlight growth in the soil carbon sector. The 'agriculture - soil carbon' method includes the ‘measurement of soil carbon sequestration in agricultural systems' method, the ‘sequestering carbon in soils in grazing systems’ method and the 'estimation of soil carbon sequestration using measurement and models' method.

Other includes energy efficiency, agriculture - other, savanna fire management, transport, industrial fugitives, facilities and carbon capture method types.

Revoked projects are excluded.

For more detail on registered projects, refer to the project register.

The method development process continues:

- Integrated farm and land management (IFLM): a draft IFLM method was made available for public consultation on 22 December 2025. The Emissions Reduction Assurance Committee (ERAC) accepted submissions between 27 January 2026 and 9 March 2026. The draft IFLM method is the first ACCU Scheme method to provide a modular framework for crediting multiple abatement activities on the same property. The method is designed to allow more activities, abatement estimation approaches, and carbon pools to be added over time.

- Improved native forest management in multiple-use public native forests (INFM): ERAC sought feedback on the proposed INFM method from 2 to 30 January 2026. The proposed method aims to generate greenhouse gas abatement by stopping or reducing harvesting in multiple-use public native forests (that is, state forests). The method was developed by the NSW Department of Climate Change, Energy, the Environment and Water and prioritised for development by the Australian Government in October 2024.

Following public consultation on each method, the ERAC will assess the method against the Offsets Integrity Standards and provide advice to the Minister.

- New savanna fire management methods remain under development with public consultation feedback being considered and final drafts of the methods for ERAC's assessment against the Offsets Integrity Standards being prepared.

- Reducing methane emission from landfill gas method was introduced by the Australian Government on 28 November 2025. The method incentivises projects to capture and destroy methane emitted from landfills as waste decomposes. It also implements Recommendation 10 of the Independent Review of ACCUs.

More information on other methods is available in the Department of Climate Change, Energy, the Environment and Water's (DCCEEW) ACCU method tracker. The tracker shows the status of ACCU Scheme methods at various stages of the method lifecycle.

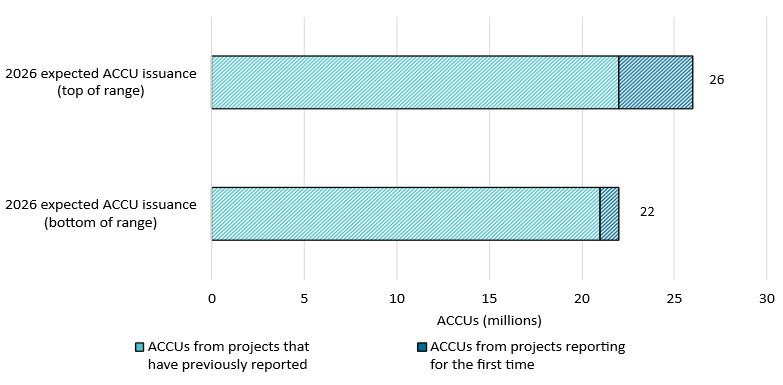

2026 ACCU issuances expected to be between 22 and 26 million

ACCU supply comprises issuances to existing projects and issuances to new projects not yet registered. While issuance from new projects will contribute to supply beyond 2026, we do not expect them to have an impact in 2026. This means expected 2026 issuances are driven by existing projects in two categories:

- Projects that have previously reported: Between 21 and 22 million ACCUs from over 600 projects that have reported in the past, with the estimate informed by project-specific historical claiming behaviour. This includes around 5.5 million ACCUs that are expected to be issued from applications on hand at the start of 2026. Our projection incorporates expected changes to the volume of ACCUs claimed on received applications.

- Registered projects expected to report for the first time: Between 1 to 4 million ACCUs. This figure involves a high degree of uncertainty because there is less information available on the volume of abatement until projects begin reporting, and the timing of first reporting is also uncertain.

The CER will refine this estimated ACCU issuance range across 2026.

Estimated Australian carbon credit unit (ACCU) issuances (in millions) in 2026

Note: This figure is not interactive.

Description

This figure shows the range of expected ACCU issuances for 2026 by category. Expected issuances were calculated using data as at 31 December 2025.

Small print

Category details:

A) ACCUs from projects that have previously reported

This is an estimate based on factors such as the typical timing and volume of ACCUs per claim. This category factors in ACCUs from applications on hand at the start of 2026.

B) ACCUs from projects reporting for the first time

This is an estimate based on factors such as the typical timing and volume of first issuance. This category is the main driver of uncertainty for the 2026 estimate.

Two notable swing factors providing the potential for issuances in the higher end of the range are:

- Human-induced regeneration (HIR) projects reporting for the first time: A large volume of HIR projects were registered in the years leading to the HIR method sunset in September 2023. Historically, the average lag between project registration and first issuance for HIR projects is around 3 years. If this pattern holds, it could translate to more HIR projects reporting for the first time in 2026. Longer times to first reporting would spread these issuances over future years.

- The new savanna fire management method under development: As discussed in the Q3 2025 QCMR, on average, credited abatement for projects under the new method is likely to be higher than under earlier savanna fire management calculators. This reflects the crediting of sequestration in additional carbon pools, enabled by improvements in scientific modelling. This may have a supply impact depending on the final method design. The CER will continue to monitor the abatement potential of these additional carbon pools as method development progresses.

Further information on our estimation approach is provided in the forthcoming Quarterly Carbon Market Report Method document. The document will summarise modelling approaches used throughout the QCMR for readers interested in more technical detail. It will be updated from time to time as methods for any QCMR analysis are updated.

Non-safeguard ACCU cancellations

Non-safeguard ACCU cancellations consist of 3 categories:

- voluntary purchases by the private or non-government sector (generally the largest category)

- compliance purchases, such as requirements for desalination plants to offset emissions

- government (non-Commonwealth) purchases, for example to offset city council emissions.

Non-safeguard ACCU cancellations have been on a downward trend since 2023. In Q4 2025, 0.4 million ACCUs were cancelled for non-safeguard demand. In total in 2025, 1.2 million ACCUs were cancelled, slightly below our estimated range of 1.3 to 1.5 million. This is a 6% decrease compared to non-safeguard demand in 2024 at 1.3 million. While voluntary cancellations rose compared to 2024, this did not offset falls of 50 to 60% in the other 2 smaller categories.

Looking ahead, CER projects non-safeguard ACCU cancellations in 2026 to be between 0.8 and 1.5 million. This is based on linear trend analysis forecasting and judgement informed by market intelligence.

Description

This figure shows ACCU non-safeguard (voluntary, compliance and government) cancellations quarterly and the annual total over time.

This figure is interactive. Hover over/tap each bar to see the quarterly ACCU cancellations in millions. Hover over/tap on the line to see the annual total of ACCU cancellations in millions. Click/tap on the items in the legend to hide/show data in the figure.

Small print

ACCU cancellations exclude deliveries against Commonwealth carbon abatement contract milestones, surrenders for safeguard purposes, and transfers to the Commonwealth Regulatory Additionality Holding Account. This classification system is uniform across ACCU and large-scale generation certificate (LGC) cancellations.

Category definitions

Voluntary

Cancellations made against voluntary certification programs and any sort of organisational emissions targets.

Compliance

Cancellations made by private organisations and corporations for compliance or obligations against municipal, local, state and territory government laws, approvals, or contracts. For example, cancellations to meet Environmental Protection Authority requirements.

Government

Cancellations by or on behalf of government entities. For example to offset emissions from vehicle fleets or meet voluntary emissions reduction targets.

Generic ACCU and SMC spot prices

The generic ACCU volume-weighted spot price fell from $37.43 at the end of Q3 2025 to $36.60 at the end of Q4, and post-quarter was sitting at $37.06 on 13 February 2026. In 2025, the generic ACCU spot price had similar seasonality to 2024 though with less volatility. Market intelligence suggests the longer-term strategies being implemented by safeguard entities has contributed to this lower volatility.

Generic Australian carbon credit unit (ACCU) and Safeguard Mechanism credit unit (SMC) volume weighted average spot price

Note: This figure is not interactive.

Description

This figure shows the volume weighted average of the generic ACCU and SMC spot prices over time.

Small print

The generic spot price refers to the daily volume weighted average price of spot trades for ACCUs with an unspecified method and spot trades for SMCs. Spot trade data is compiled from trades reported by Jarden and CORE markets, and may not be comprehensive. Prices are shown from 31 December 2020 to 13 February 2026. The last quarterly and data cut off reported daily volume weighted average spot prices for generic ACCUs and SMCs are labelled.

SMC prices continue to follow generic ACCU prices. Given the low volume of spot trades for SMCs, firm conclusions about the ACCU-SMC price differential should be viewed with some caution. The SMC volumeweighted spot price fell from $37.00 at the beginning of Q4 2025 to $35.80 at the end of Q4 2025. The price differential between SMCs and ACCUs tightened during Q4 2025 almost reaching parity at the end of 2025. In early 2026, SMCs have consistently traded for around $0.05 below the generic ACCU spot price.

Nature Repair Market update

Reforms to the Environmental Protection and Biodiversity Conservation (EPBC) Act passed on 28 November 2025 included amendments to the Nature Repair Act 2023 to allow for methods to specify whether biodiversity offsets could be used as environmental offsets. The Nature Repair Market will continue to support voluntary action on nature repair. Not all Nature Repair Market projects will be used as environmental offsets and a proponent can choose whether their certificate is used as an offset.

The first method under the Nature Repair Market (released early 2025) supports landholders to undertake projects to enhance biodiversity by replanting native forest and woodland ecosystems on historically cleared landscapes. Biodiversity certificates under this method cannot be used as regulatory environmental offsets.

The proposed protect and conserve and enhancing nature vegetation methods continue to be developed. The Nature Repair Committee plan to undertake statutory consultation on the final proposed methods in 2026 to inform their advice to the Minister for the Environment and Water.

Integrity and transparency update

The CER published the annual NGER datasets and register on 27 February 2026. This includes corporate emissions and energy data, electricity sector emissions and generation data and the name of each person that registered the previous reporting year.

As part of our ongoing work to increase transparency and provide carbon markets with more information about the schemes we administer, we:

- consulted on improvements to the ACCU and contract register and plan to release the results of the consultation in April 2026. In Q4 2025, the CER consulted on improvements to register. Submissions were open from 17 November to 19 December 2025. The CER is undertaking work to improve the content and presentation of the register in 2026. This includes migrating the register to data services and changing the data. The consultation aimed to ensure the proposed changes will meet data user needs.

- published a preliminary overview of Safeguard Mechanism outcomes and key market data for the 2024-25 reporting period. This new publication provides important indicative information on scheme outcomes ahead of the full compliance year data that we will publish on 15 April 2026.

- have extended the historic time series for many figures in the QCMR data workbook, including all ACCU figures. We will continue to add more historical data to the workbook over time.

- are publishing a QCMR Methods document (forthcoming) to provide interested stakeholders with more technical information about the data and methods used in the QCMR.

- have created a consolidated list of compliance dates and key data releases for all CER schemes. See the appendix in the downloadable report (1.8 MB pdf).