This chapter is included in each Q4 QCMR and functions as the basis for the annual Renewable Energy Target’s administrative report. It consolidates material in the chapters on the Large-scale Renewable Energy Target (LRET) and Small-scale Renewable Energy Scheme (SRES) and places these in context of the Australian Government’s wider suite of electricity sector policies.

Investment in renewables is supported by the Renewable Energy Target (RET) through large-scale generation certificates (LGCs) and small-scale technology certificates (STCs). LGCs and STCs provide incentives to bring forward investment in additional renewable energy and the consequential reduction in greenhouse gas emissions.

2024 saw Australia’s rollout of renewable energy generation capacity reach new heights, with a record 7.5 gigawatts (GW) of renewable energy capacity being added over the year. This consisted of 4.3 GW of approved large-scale power stations (also a record year) and around 3.2 GW of small-scale rooftop solar installations (the latter equals the pandemic induced record in 2021). For the second year in a row, households and businesses also installed more than 100,000 air source heat pumps (energy efficient hot water systems).

In 2024, the total estimated generation incentivised by the SRES and LRET was 32,400 gigawatt hours (GWh) and 50,100 GWh respectively, for a total 82,500 GWh. This represented around 32% of all electricity generation in Australia, nearly 4% higher than 2023. The total amount of renewable generation includes hydro and other baseline renewables not eligible for LGCs. Across both the National Electricity Market (NEM) and Western Australia’s South West Interconnected System (SWIS) ((NEM+SWIS)), renewable generation was 92,700 GWh in 2024.

While total generation incentivised by the SRES and LRET increased from 2023 to 2024, the total renewables share in the NEM+SWIS remained unchanged at 39% because of a shortage of water for hydro generation and a wind drought experienced through late autumn to early winter. Renewable penetration in the NEM was particularly strong in Q4 2024 at 46% and continues to make a strong showing in early 2025.

In 2025, an estimated 2.9 GW to 3.2 GW of rooftop solar is expected to be added to the grid.

- Trends from later in 2024 and January 2025 suggest that the actual capacity may currently be heading for the top end of this range. The lower bound on rooftop solar is based on modelling from consultants prepared in mid-2024 to inform the small-scale technology percentage (STP) for 2025. The drivers of rooftop capacity are discussed further in chapter 4.

At this stage, a conservative view of additional large-scale renewable energy capacity in 2025 is around 2.7 to 3.1 GW. We will progressively update this estimate during the year as we track progress of construction and expected first generation dates.

- LRET applications totalling 1.7 GW of capacity are currently under assessment by the CER which forms a strong starting point for 2025.

- The timing of final investment decision (FID) and first generation for large renewables projects are inherently lumpy. Since 2019, between 3 and 3.5 GW of capacity has reached FID each year on average, while an average of less than 3 GW has been approved for LGC creation. This sustained gap was part of the reason for the record 4.3 GW approved in the 2024 year and could mean a higher capacity accredited this year or next. However, estimating the timing of large projects reaching first generation is subject to a range of uncertainties. For example, construction timelines can be affected by weather, workforce shortages and supply chain issues.

Description

This figure shows installed capacity under the SRES and approved capacity for wind and solar power stations under the LRET in gigawatts (GW) over time.

This figure is interactive. Hover over/tap each segment to see the capacity. Click/tap on the items in the legend to hide/show data in the figure.

Small print

A 12 month creation period for registered persons to create small-scale technology certificates (STCs) applies under the Renewable Energy (Electricity) Regulations (2001). SRES installed capacity in 2023 and 2024 has been lag-adjusted to account for the 12 month creation rule and is an estimate only. Installed capacity is subject to change.

Capacity figures relating to the LRET are based on the approval date. This is the date a renewable energy power station was approved by the Clean Energy Regulator to be accredited to generate large-scale generation certificates (LGCs). This chart does not include approved capacity for biomass and hydroelectric power stations, which are a small component of overall approved capacity.

SRES makes strong contribution to the renewable energy transition

Rooftop capacity installed in 2024 has exceeded 2023 capacity, despite a marginal drop of around 14,000 overall installations to 320,000. The rise in installed capacity is due to the increase in the average installed system size. The average capacity of solar PV systems installed in 2024 was 10.0 kW, an increase of 0.6 kW compared to 2023.

Batteries are also being installed with solar systems more frequently. Figures reported to the CER show that around 10% of rooftop solar systems installed in 2024 were connected to a battery. This is up from 8% in 2023. Battery installations are not covered under the SRES, so this data is reported on a voluntary basis. It is very likely that the proportion of systems being installed with a battery is higher. Increasing volumes of storage will be important to ensure more generation from rooftop solar can be used rather than being curtailed or leading to the curtailment of other renewables by network operators to maintain power system security.

Since 1 January 2020, 15.3 GW of rooftop solar capacity has been installed. This is nearly 60% of the total small-scale capacity installed since the SRES commenced in 2001. At the time of writing, 2024 was possibly a new annual record. However, due to the lag in certificate creation this will not be clear until around April when the bulk of December 2024 certificates are expected to have been created.

Industry analysts have reported a global oversupply of solar panels in 2024, attributing this to the introduction of new panel technology. This is a contributing factor to the fall in system prices over the course of 2024, from around $0.96 per watt in late 2023 to around $0.90 per watt in February 2025. The CER estimates that the average payback period for a new small-scale solar system has decreased from 4 years in late 2023 to approximately 3.5 years as of the end of 2024. This estimate uses the same method and assumptions as in the Q3 2023 QCMR with updated data.

Record year for large-scale renewables with strong future pipeline

In 2024, the CER approved 548 large-scale renewable power stations totalling 4.3 GW of capacity to create LGCs under the RET. This was a significant uplift from the 2.2 GW approved in 2023 and marks a new record for new capacity approved in a single calendar year. Headlining the new capacity added in 2024 were the two largest large-scale renewable power stations in Australia – MacIntyre Wind Farm (923 megawatts ((MW)), and the Golden Plains Wind Farm East (756 MW). For the first time since 2020, Victoria led the nation in new large-scale capacity, with 32% of the capacity approved in 2024. Queensland and New South Wales contributed 24% and 23%, respectively.

In addition to the record-setting year for approved large-scale capacity, 2024 was a strong year for investment in renewables. Utility-scale wind and solar projects totalling 4.3 GW of capacity reached the FID phase of development within the year.

As discussed above, it is difficult to accurately predict exactly when capacity that has reached FID will be available to the grid given substantial uncertainties associated with construction and connection timelines. At this stage, a conservative view of additional large-scale renewable capacity in 2025 is around 2.7 to 3.1 GW. Utility scale renewables take a minimum of 12 months from commencing construction to reach first generation of electricity, with some projects taking considerably longer. These extended lead times understandably correlate with increasing project sizes. The CER will update this estimate throughout the year.

The recent announcement from the Capacity Investment Scheme (CIS) also support a strong outlook for renewables. This potential impact of the announcement is discussed later in the chapter.

Renewables penetration stable in 2024, but material lift expected in 2025

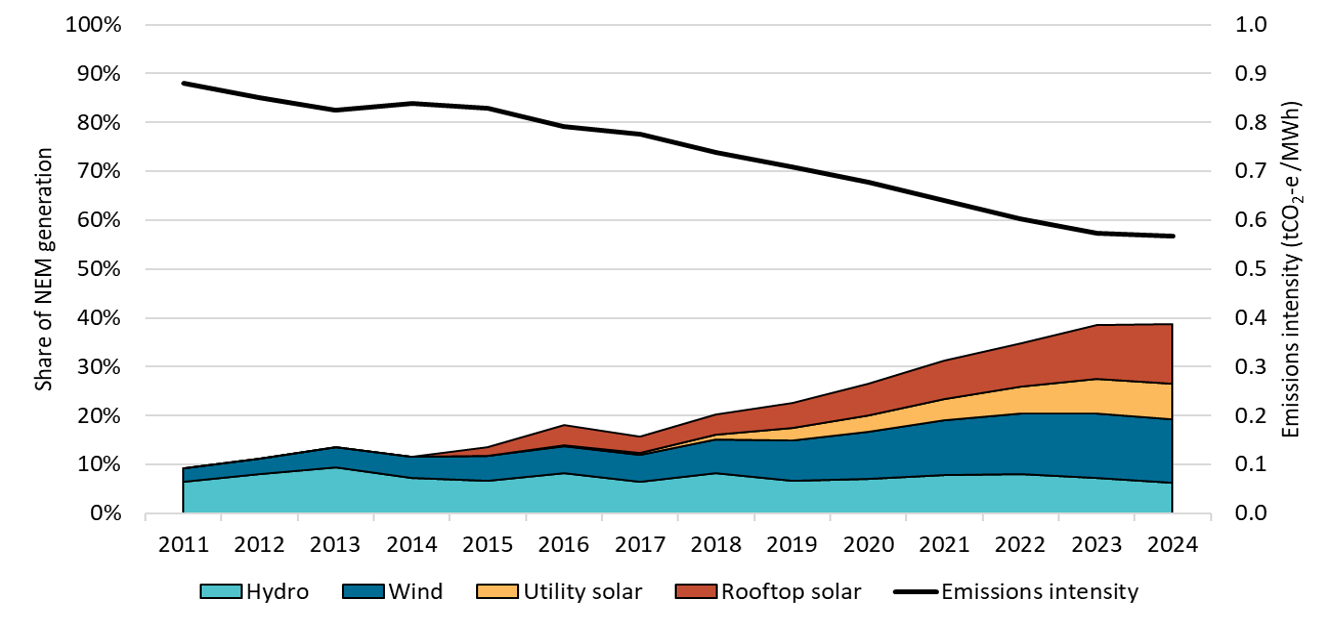

The Australian Government has a target of 82% renewable electricity nationally by 2030. We would generally expect a year-on-year increase of more than 3% as a reflection of annual capacity being added to the grid. However, renewables’ share of generation in the NEM in 2024 remained at the 2023 level of 39%.

- This result is largely attributed to a wind drought experienced through late autumn to early winter and weaker-than-expected generation from hydroelectricity plants due to below-average rainfall in Tasmania.

- Australian Energy Market Operator (AEMO) data from the August 2024 Engineering Roadmap and more recently in the latest Quarterly Energy Dynamics (QED) report indicate that economic offloading and network curtailment of renewables is also likely to have made some contribution the result. Whether in response to low or negative wholesale prices (economic offloading) or to power system security requirements (network curtailment), material levels of curtailment mean existing renewable assets are not generating as much electricity for consumers as they could if more electricity could be stored or transmitted. The suite of Australian Government policies increasing both large-scale storage and transmission already in train, coupled with AEMO’s work to reducing technical and engineering barriers to high renewables penetration, will facilitate greater use of existing assets.

- On the demand side, there was also material increase in the overall electricity demand in the NEM (3.0% compared to between 0.2% and 1.8% over the previous 3 years).

In combination, these factors resulted in the proportion of renewables generation in the NEM remaining stable. Only rooftop and large-scale solar saw growth in their generation contributions to the NEM in 2024 – by 9.5% and 5.5% respectively compared to 2023.

The emissions intensity of the NEM remained stable in 2024 compared to 2023, at 0.57 tonnes of carbon dioxide-equivalent per megawatt-hour (MWh) of generation. Further information on emissions from electricity is available in the 2023-24 NGER data release.

In January 2025, the AEMO released the Quarterly Energy Dynamics (QED) report for Q4 2024. The report highlighted that small-scale solar output reached an all-time quarterly high in all regions, driving a record share of 46% of supply in the NEM from renewable sources. The QED report also detailed a half-hourly snapshot where renewable contributions to the NEM reached an all-time high of 75.6% on 6 November 2024.

The CER anticipates that renewable penetration in the NEM could reach 44% to 46% in 2025. This range assumes a return to average generation conditions, particularly for wind and hydro. It also assumes no material increases in curtailment or electricity demand growth.

Renewables generation share and emissions intensity of the National Electricity Market

Note: This figure is not interactive.

Description

This figure shows the share of generation contributed by renewables in the National Electricity Market (NEM) over time. It also shows the emissions intensity of the NEM as tonnes of carbon dioxide-equivalent (t CO2-e) per MWh over time.

Small print

Generation and emissions intensity data of the NEM sourced from OpenNEM on 31 January 2025. The NEM operates in ACT, NSW, Qld, SA, Vic and Tas. It does not include WA or NT. A small portion of renewable generation from biomass is not shown.

Capacity Investment Scheme poised to drive rise in large-scale generation and storage

On 11 December 2024, the successful projects under CIS Tender 1 of the CIS were announced. Successful projects are still subject to the signing of a Capacity Investment Scheme Agreement (CISA) with the Australian Government.

The successful projects consisted of a total 19 projects with a combined 6.4 GW of generation capacity and around 3.6 GWh of storage capacity. Solar projects made up 2.8 GW of the generating capacity, with wind projects making up the remaining 3.6 GW. The total 6.4 GW exceeded the indicative target generation capacity by 0.4 GW. Reflecting the increasing importance of dispatchable power to the renewable energy transition discussed above, 8 of the 19 successful CIS projects were hybrid generation and storage projects.

We would expect revenue underwriting agreements available to projects supported through finalised CIS contracts will increase the likelihood of reaching financial milestones such as FID in a reduced timeframe. Given the sizeable capacity of successful bids in Tender 1, total capacity reaching FID in 2025 could be around 6 GW or potentially more, noting announcements from further CIS rounds are scheduled from next month.

- Successful bids under Tender 2 – Wholesale Electricity Market (WEM) Dispatchable of the CIS are scheduled to be announced in March 2025. Tender 2 is seeking to deliver 2 GWh of storage capacity in the SWIS.

- There are also two further tenders underway – Tender 3 – NEM Dispatchable Capacity, aiming to deliver 4 GW of four-hour equivalent dispatchable capacity, or 16 GWh of dispatchable capacity in the NEM, and Tender 4 – NEM Generation, aiming to deliver a further 6 GW of renewable generation capacity in the NEM. Project bids for Tender 3 closed on 18 December 2024, and successful bids are expected to be announced in September 2025, while project bids for Tender 4 closed on 18 February 2025, and successful bids are indicatively scheduled to be announced in October 2025.