On this page

- Market dynamics

- Record volume of approved large-scale capacity

- Strong end to year for final investment decisions

- Voluntary (non-RET) LGC Holdings increase in Q4

- Supplementary figures

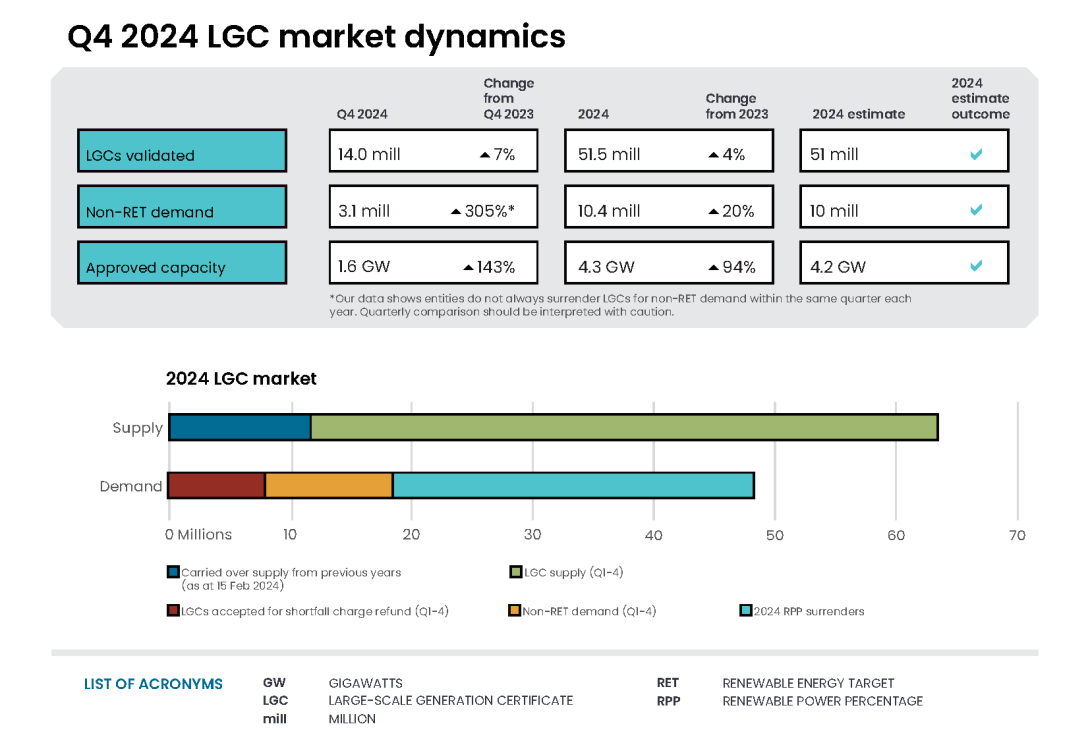

Market dynamics

Table 3.1: Large-scale generation certificate (LGC) supply and demand balance

| Demand | Supply | |

|---|---|---|

| Supply carried over from previous years (as of 15 Feb 2024) | 11.9 million | |

| LGC supply (Q1-4 2024) | 51.5 million | |

| Non-RET demand (2024) | -10.4 million | |

| 2024 RPP surrenders | -30.2 million | |

| LGCs accepted for shortfall charge refund (Q1-4 2024) | -7.5 million | |

| Estimated balance as of 15 Feb 2025 | 21.1 million | |

Note: There is a total of 4.3 million LGCs in shortfall that are eligible for shortfall refunds to be claimed from 2022. There is $800 million in consolidated revenue (representing 12.3 million LGCs) from shortfall charges that are eligible for redemption as of 15 February 2025.

In Q4 2024, 14.0 million LGCs were created, bringing total LGC creations to 51.5 million for the year. This volume was in line with updated projections in the Q3 2024 QCMR. Assuming weather conditions are favourable throughout 2025, it is reasonable to expect 54 to 57 million LGCs to be created in the year.

The 14 February surrender deadline saw 30.2 million LGCs surrendered against a total liability of 34 million. Shortfall totalling 3.8 million LGCs was taken by 6 liable entities, with an additional 0.4 million in liability carried forward to next year’s deadline by 17 liable entities.

Additional factors to consider in the LGC market throughout 2025 will be the impact of the introduction of mandatory climate disclosures and a material uplift in voluntary cancellations. These are discussed further below.

Description

This figure shows the number of LGCs validated by technology type over time.

This figure is interactive. Hover over/tap each segment to see the number of LGCs. Click/tap on the items in the legend to hide/show data in the figure.

Small print

Waste coal mine gas is no longer eligible to create LGCs as of 2021. Validations in 2021 reflect LGCs that were created prior to 2021.

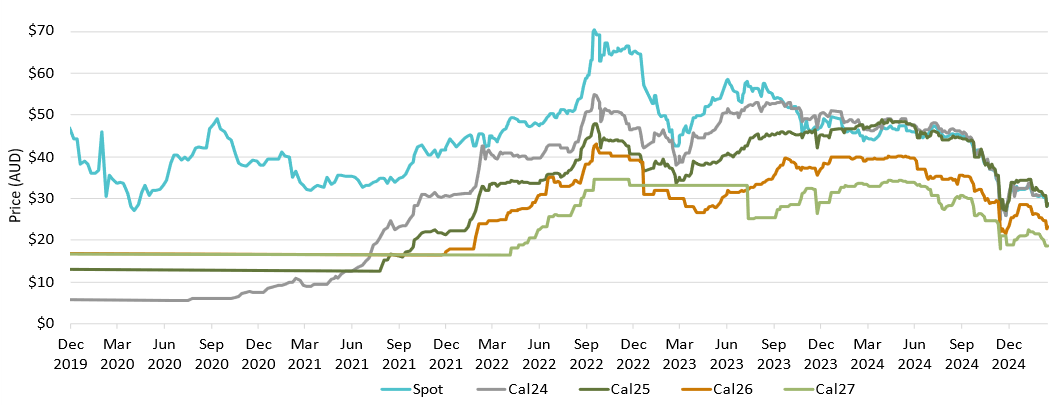

The LGC spot price experienced a sharp decline in mid-Q4 with a partial recovery later in the quarter. The spot price dropped from $41.50 at the start of Q4 to a low of $26.00 in late November, before rebounding to finish the year at $32.25. The LGC spot price has settled at around $28 since the 14 February surrender deadline.

It is difficult to quantify the absolute uplift in non-RET demand at this stage, but the CER expects a material uplift in surrenders. It would not be extreme to expect between 12.5 and 15 million LGCs could be surrendered for non-RET purposes in 2025. This is likely to be a factor influencing the Cal25 futures which were trading at $29.00 on 18 February. The CER has been informed that some entities with 100% renewable energy targets in FY2025 will be surrendering in Q3 2025. Early indications suggest that meeting these commitments could require an up to 4-fold increase in cancellations for some entities. The phased introduction of mandatory climate disclosures from 1 January will see the corporate disclosures in a new sustainability report. While disclosures do not create new emissions reduction requirements, the reporting requirements could increase interest in voluntary retirement of LGCs or other certificates. The CER will continue to consult with relevant entities throughout the year to refine this estimation.

Despite the uplift in voluntary demand, overall LGC supply (stock and expected creations) is still expected to readily account for demand coming from both RET and non-RET surrenders. This includes the 4.3 million currently eligible for shortfall refund.

Large-scale generation certificate (LGC) reported spot and forward prices

Note: This figure is not interactive.

Description

This figure shows the daily closing LGC spot price and calendar year forward prices over time.

Small print

For example, Cal25 is the 2025 calendar year, where an agreement is made to buy/sell LGCs at a specified price in 2025. Pricing data is compiled from trades reported by CORE markets and may not be comprehensive. Prices are shown from 1 December 2019 to 14 February 2025.

The 2025 renewable power percentage (RPP) has been set at 17.91%. The RPP is set by the Minister for Climate Change and Energy each year to meet the LRET’s annual legislated target for renewable electricity which is 33,000 GWh each year from 2020 to 2030. Given the legislated target for renewable electricity is fixed, recommended RPPs tend not to vary much from year to year. The 2025 RPP is marginally lower than 2024 and will require liable entities – typically electricity retailers – to surrender approximately 32 million LGCs. The small decrease from the 33 million target in the 2025 RPP calculation reflects a rolling adjustment to account for over surrenders in previous years.

Record volume of approved large-scale capacity

Approved capacity in Q4 2024 under the LRET was very high with 1.6 GW of capacity approved during the period. This was driven by the approval of Australia’s largest wind farm – MacIntyre Wind Farm (923 MW), as well as Walla Walla Solar Farm 1 and 2 (353 MW).

This outcome has resulted in a record 4.3 GW of renewable energy generation capacity being approved in 2024 – exceeding the previous record of 4.2 GW set in 2020, and nearly doubling the 2.2 GW of capacity approved in 2023.

Description

This figure shows the capacity of large-scale wind and solar power stations approved by the Clean Energy Regulator to generate large-scale generation certificates over time.

This figure is interactive. Hover over/tap each bar to see the capacity. Click/tap on the items in the legend to hide/show data in the figure.

Small print

Solar and wind hybrid projects are grouped under the solar category. Totals may not sum due to rounding.

2.4 GW of wind capacity was approved in 2024. For the first time since 2020, wind power made up the bulk of approved power stations in a calendar year. This is a significant metric as wind assets tend to have higher capacity factors and often generate significant energy at night. Solar assets also make a valuable contribution to the energy mix through reduced prices during daylight hours. The development of storage assets in the network will serve to reduce energy prices in high price periods as generation from wind and solar assets can be stored and shifted to meet demand as needed.

There is currently 1.7 GW of large-scale capacity under assessment by the CER. This suggests that the first half of 2025 could carry forward the strength in approvals seen in 2024.

Strong end to year for final investment decisions

2024 investment ended strongly, with 1.3 GW of capacity reaching Final Investment Decision (FID) in Q4. Total capacity to reach FID in 2024 was 4.3 GW.

Significant projects reaching FID in Q4 2024 include:

- Goulburn River Solar Farm (450 MW)

- Wambo Wind Farm – Stage 2 (254 MW)

- Wambo Wind Farm – Stage 1 (250 MW)

- Carwarp Solar Farm (150 MW)

- Horsham Solar Farm (119 MW)

- Warradarge Wind Farm (108 MW).

Goulburn River Solar Farm reached FID following the announcement of its successful bid under Tender 1 of the Capacity Investment Scheme (CIS).

A total of 19 large-scale projects totalling 6.4 GW of generation and 3.6 GWh of storage capacity were successful in the first round of the CIS. The rate at which these project reach generation stage will vary. While a few are further advanced in the development cycle and could see accreditation under the LRET within 18 months, others will take more time.

Description

This figure shows the capacity and four quarter rolling average of large-scale renewable power stations to reach a final investment decision over time.

This figure is interactive. Hover over/tap each bar to see the capacity. Hover over/tap along the line to see the rolling average. Click/tap on the items in the legend to hide/show data in the figure.

Small print

The Clean Energy Regulator tracks public announcements. Data may be incomplete and may change retrospectively. Totals may not sum due to rounding. Data as at 31 December 2024.

Voluntary (non-RET) LGC Holdings increase in Q4

LGC holdings increased by 10.7 million to 46.0 million at the end of 2024, up from 42.9 million at the end of 2023. Holdings by voluntary participants at the end of 2024 were nearly double that at the end of 2023 (4.4 million in 2023 and 8.2 million last year).

Description

This figure shows LGC holdings in Renewable Energy Certificate (REC) Registry accounts by market participation category over time.

This figure is interactive. Hover over/tap each data point to see the number of LGCs in millions. Click/tap on the items in the legend to hide/show data in the figure.

Small print

Holdings are for registered LGCs as at the end of the quarter and exclude any pending transactions. Accounts are categorised according to their primary role or function based on transaction patterns and the name of the account. An account's category is subject to change. Totals may not sum due to rounding.

Category definitions

Liable entity

Account holder is a liable entity.

Power station

Account holder has created LGCs.

Non-RET (voluntary)

Account holder has surrendered LGCs voluntarily. This includes accounts labelled as 'GreenPower' in the REC Registry.

Non-RET (compliance)

Account holder has surrendered LGCs voluntarily for non-RET compliance reasons (for example, desalination plants) or the account holder is a Safeguard entity or related to a Safeguard entity.

Non-RET (government)

Account holder has surrendered LGCs voluntarily and is a government entity.

Intermediary

Account holder has transacted/received over 1 million LGCs and does not fit into any of the other categories.

Other

Account holder does not fit into any of the other categories.

Non-RET surrenders totalled 3.1 million LGCs in Q4 2024, bringing the annual total to a record 10.4 million. This was 20% higher than the 8.7 million surrenders in 2023. As discussed above, consistent with the substantial growth in non-RET holdings late last year, non-RET LGC surrenders in 2025 are expected to exceed those in 2024.

Description

This figure shows non-RET LGC cancellations by demand source over time.

This figure is interactive. Hover over/tap each segment to see the number of LGCs. Click/tap on the items in the legend to hide/show data in the figure.

Small print

This classification system is uniform across Australian carbon credit unit (ACCU) and LGC cancellations.

Covered activities for each classification

Voluntary demand

Cancellations made against voluntary certification programs such as Climate Active and any sort of organisational emissions or energy targets.

Government demand

Cancellations by or on behalf of government entities. For example to offset emissions from vehicle fleets or meet voluntary emissions reduction targets.

Compliance demand

Cancellations made by private organisations and corporations for compliance or obligations against municipal, local, state and territory government laws, approvals, or contracts. For example, to meet Environmental Protection Authority requirements.

Supplementary figures

Large-scale generation certificate (LGC) spot price

Note: This figure is not interactive.

Description

This figure shows the daily closing LGC spot price over time.

Small print

Spot price data is compiled from trades reported by CORE markets and may not be comprehensive. Prices are shown from 1 December 2019 to 14 February 2025.