Understanding the timeline of an Australian Carbon Credit Unit (ACCU) Scheme project can help you better understand how carbon abatement is calculated and how ACCUs are generated.

Within this timeline, there are key dates and timeframes:

- the baseline period

- the crediting period

- a permanence period (for sequestration projects)

- reporting periods

- the model start date (for sequestration projects)

- audit schedules.

Each of these have specific definitions that ensure carbon abatement is calculated accurately and ACCUs are issued incrementally.

Baseline period

The baseline period establishes the project area conditions as they exist before carbon abatement activities start. This is necessary to determine the amount of carbon emissions or sequestration that would have occurred without the project.

The baseline period helps to ensure that:

- project activities lead to abatement that wouldn’t have occurred otherwise

- there’s a benchmark for measuring emissions reduction or sequestration across the project’s life

- the project meets key eligibility requirements.

Crediting period

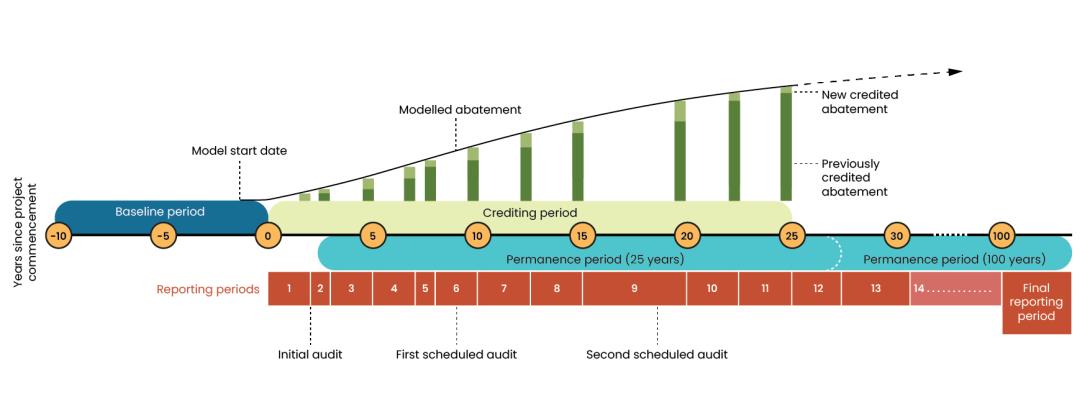

A crediting period is how long an ACCU Scheme project can generate and claim ACCUs. It is generally 7 years for emissions avoidance projects and 25 years for sequestration projects.

The crediting period start date is either:

- decided by the project proponent when they register a project and must generally be within 18 months from the registration date

- set to start when we register the project.

After registration, the project proponent may subsequently vary the project’s start date to a date not later than 18 months after registration (although for some methods, a longer period is allowed). Projects registered before 30 June 2015 follow additional rules.

During the crediting period, carbon abatement delivered and reported above any baseline level is incrementally credited as ACCUs.

ACCU issuances may be paused during a project’s crediting period if:

- the project fails to deliver any abatement above baseline levels during a reporting period

- measurement or modelling show a decline in abatement compared with previously issued levels.

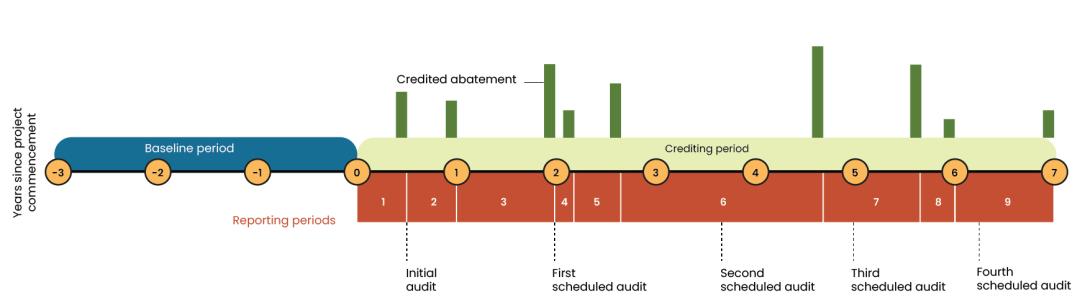

Example project timeline for an emissions avoidance project

Reporting period

A reporting period is the timeframe covered by an offsets report regarding the activities of a project. The length of the reporting period varies based on the type of project. Project proponents can choose the length of a reporting period within fixed limits. This reporting period is usually between 6 months to a maximum of 5 years.

All projects must submit offsets reports throughout the entire crediting period. Some sequestration projects must also continue to submit offsets reports for the duration of the permanence period.

Regular project reporting helps to maintain integrity in the scheme by demonstrating that a project is being managed appropriately. We assess the information and evidence provided in proponent’s regular offsets reports and in independent audit reports. This provides strong assurance that projects only receive ACCUs for proven abatement.

Find out more about integrity and transparency in the ACCU Scheme.

Extended accounting periods

Some methods have an extended accounting period, which begins when the crediting period ends. During this period, projects can report and earn ACCUs for abatement calculated and accrued in the crediting period. Activities conducted during the extended accounting period aren’t eligible to earn ACCUs.

Audit schedule

All projects are issued with an audit schedule at registration. The number of scheduled audits is based on the project’s size and the average annual abatement it’s expected to generate. For most projects, we schedule at least 3 audits during the crediting period.

All audits need to establish reasonable assurance that the abatement achieved and reported on by a project is accurate.

Read more about audits and how they relate to project reporting.

Permanence period

Project proponents elect their permanence period when applying to register a sequestration project. The duration of the permanence period can be 25 or 100 years.

The permanence period start date begins on the date that the project is first issued ACCUs and will be reset if area is later added to the project.

During the permanence period, the project proponent must maintain the level of carbon stored by the project and prevent carbon release back into the atmosphere.

If there is a significant reversal event (such as a bushfire) that the project proponent has caused or has improperly managed, the project may be required to relinquish ACCUs to offset the loss.

Example project timeline for a sequestration project

Model start date

The model start date is only used in vegetation methods that use the Full Carbon Accounting Model (FullCAM) or the Reforestation Modelling Tool (RMT). It is the date when modelling begins in a specific carbon estimation area.

The model start date is a key input in the model and represents the date when modelling begins in a specific carbon estimation area. In some methods, a model start date can occur before the crediting period start date. Depending on the method, carbon abatement that occurs before the crediting period start date may or may not be credited. For example, projects under the avoided clearing of native regrowth method are credited for maintaining and not clearing the vegetation that grew before the project was registered.

The use of a model lowers the cost of estimating abatement. Specific eligibility criteria and regular checks and audits throughout the life of a project ensure that the model is only applied to areas of eligible land that are appropriate for the model.

Aside from the model start date, carbon abatement modelling will also factor in management activities, disturbance events and growth pauses events. This ensures that ACCU issuance accurately reflects the levels of carbon sequestration experienced in the project.

About FullCAM

FullCAM is a computer modelling tool developed by the Department of Climate Change, Energy, the Environment and Water (DCCEEW) and supported by the CSIRO.

It estimates changes in carbon stock, such as biomass in trees and woody debris, depending on the type of planting or regeneration system being modelled. The model is informed by calibration plots taken from a range of ecosystems across Australia.

Projects registered under some earlier methods may use the RMT to calculate the carbon abatement of their projects.